Report: Indonesia’s just energy transition partnership

The Indonesia Just Energy Transition Partnership (I-JETP) is a landmark climate finance agreement reached between Indonesia and a group of…

The Sixth Assessment, Working Group III (AR6 WGIII) report was released in April 2022, providing the most comprehensive review of how we can mitigate climate change since the Fifth Assessment (AR5) in 2014 and the IPCC’s three recent special reports (SR1.5 in 2018 and the 2019 SRCCL and SROCC).

Keeping the global average temperature increase to 1.5°C will require major energy system transformation, including substantial reduction in overall fossil fuel use and widespread electrification with net-zero or net-negative emissions electricity systems (SPM C.4, C.4.1). Illustrative mitigation pathways suggest the year for net-zero CO2 emissions is typically around 2050 (chapter 3, cross-chapter box 3).

The transition to a net-zero economy requires significant investments across the global economy, with wind and solar expected to dominate low-carbon generation and capacity growth over the next two decades (chapter 6.7.1.2). Solar and wind have grown 170% and 70%, respectively, from 2015-2019 (chapter 6, executive summary). Since 2010, the sustained fall in the cost of solar energy (85%), wind energy (55%) and lithium-ion batteries (85%) has made renewable energy cheaper than fossil fuels in many regions (chapter 6.4). In scenarios that limit warming to 1.5°C with no or limited overshoot, low- or zero-carbon sources of energy will produce 97%-99% of global electricity by 2050, as global electricity demand doubles by 2050 (chapter 6.7.1.2). The share of solar and wind in electricity generation could reach as high as 40% by 2030, and nearly 70% by 2050 (chapter 6, figure 6.30).

The massive shift to renewable energy generation and electrification of end uses will require significant increases in global energy investments. In 2019, global energy investment was approximately USD 1.9 trillion, of which half (USD 990 billion) was spent on fossil fuels (chapter 6.7.2). In the future, limiting warming to 1.5°C with no or limited overshoot will require between USD 2.4 trillion to 4.7 trillion in annual global energy investments between 2016-2050 (chapter 6.7.2). In the near-term, the IPCC estimates that annual investment in electricity supply between 2023-2032 will need to reach the following amounts (chapter 15, table 15.2):

The global economic benefit of limiting warming to 2°C exceeds mitigation costs under most assumptions (SPM C.12.3). Given the cost reduction in key technologies, such as renewable energy and electric vehicles, maintaining carbon-intensive systems is already more expensive than transitioning to low carbon systems in some regions (SPM C.4.2; chapter 6.7). Current models that quantify the macroeconomic implications of climate mitigation do not account for reduced adaptation costs or economic damages from climate change, which can destroy lives, livelihoods, property and infrastructure (SPM C.12). There is also a large variation in the effect of mitigation on GDP across regions, and overall, the effect of mitigation on GDP is small compared to growing GDP, which is projected to at least double over 2020-2050 (SPM C.12.2). When climate impacts are considered, lack of mitigation will lead to significant economic damages leading to greater falls in GDP, according to the AR6 Working Group II report (WGII report, chapter 16). In a literature review of studies that estimate global economic impacts at differing degrees of warming, the WGII report found that warming of up to 2°C could mean up to 35% annual loss in global GDP (chapter 16, cross-working group box economic.1). Scenarios with earlier mitigation action tend to bring higher long-term GDP than scenarios that delay action to the end of the century (WGIII, chapter 3.6.1).

Economic growth no longer means emissions growth for an increasing number of countries around the world (chapter 2.3.2). In assessing how emissions occur, consumption based emissions (CBE) is a common metric for understanding to what extent consumption choices can influence climate mitigation targets (chapter 2.3.1). Between 2015 and 2018, 23 out of 116 countries achieved absolute decoupling of CBE to GDP. Most EU and North American countries are in this group, with decoupling achieved not only by outsourcing carbon intensive production but with improvements in production efficiency and the energy mix, leading to a decline of emissions (chapter 2.3.3, table 2.3). Also, 67 countries representing 58% of the world’s economy, including China and India, have seen GDP growth begin to decouple from consumption-based GHG emissions growth. In other words, consumption-based emissions growth slowed, relative to GDP growth, during 2015 to 2018 (chapter 2.3.3).

Accelerated international financial cooperation is a critical enabler of low-GHG and just transition to address inequities in access to finance and cost of impacts (SPM E.5). Climate cooperation can generate economic benefits, both in large developing economies (India, China) and industrialised countries, such as in Europe (chapter 3.6.1.2). Additional cooperation mechanisms like trade, technological diffusion, and finance can deliver cost savings and improve equity in the transition (chapter 3.6.1.2).

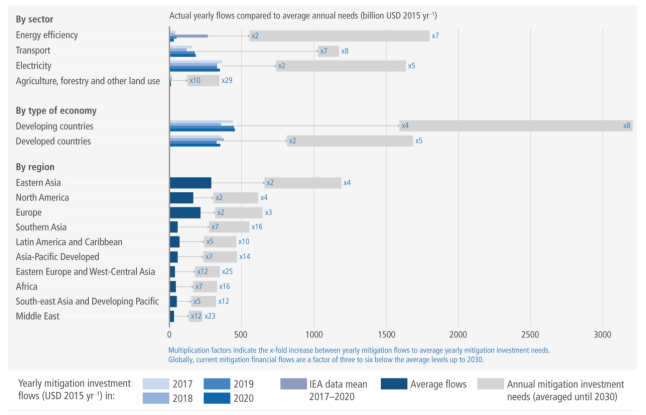

Although the renewable energy sector attracted the highest level of funding in recent years, a stable annual investment gap remains between current levels of investment and what is needed to achieve a net-zero energy system (chapter 15.5.2). Figure 15.4 in the IPCC report illustrates the significant need to increase funding in all sectors and regions, as follows:

A large gap also exists in the flow of finance needed to support a global energy transition in emerging and developing economies. Over 80% of climate finance (broadly defined as finance flowing to cutting emissions or adapting to climate change) is reported to originate and stay within borders. This figure rises to over 90% for private finance, while finance flows remain unevenly distributed across regions and sectors (chapter 15.5.2).

Ongoing investments in coal and other fossil fuel infrastructure risks locking in higher emissions, making it impossible to achieve 1.5°C (chapter 6, box 6.13). Limiting warming to 1.5°C would require a combination of decommissioning, retrofitting and reduced use of existing fossil fuel energy sources, as well as the cancellation of any new infrastructure (SPM B.7.2). The use of coal, oil and gas without CCS is projected to fall by 100%, 60% and 70%, respectively, by 2050 (SPM C.3.2), potentially costing taxpayers, energy users, and investors trillions of dollars in stranded assets (chapter 15.3.3). Limiting warming to 1.5°C would require coal- and gas-fired power plants to retire 30 years earlier than in the past – historically they have operated for on average 39 and 36 years, respectively (chapter 6, box 6.13).

While CO2 emissions from fossil fuels are significantly reduced in scenarios that limit warming to 1.5°C or below than 2°C, around 800-1000 GtCO2 of net cumulative CO2 emissions remain (chapter 3, box 3.4). As such, creating net-negative emissions will need to be a part of mitigation strategies to achieve net zero. Although the IPCC recognises that carbon dioxide removal (CDR) is necessary to achieve net-zero GHG globally, it should only be deployed to balance hard-to-abate residual emissions (e.g. aviation, agriculture and industrial processes) (SPM C.11.4). The IPCC generally identified three CDR methods – biological removal (such as afforestation, bioenergy carbon capture and sequestration, biochar, ecosystem restoration and ocean fertilisation), geochemical removal (such as enhanced weathering) or chemical removal (such as direct air capture and storage) (SPM C.11.1). There is uncertainty about how much CDR will be deployed in the future, given feasibility and sustainability constraints (chapter 12.3).

Some of the concerns with large-scale CDR deployment include:

This means that immediate emissions reduction should be the focus of mitigation action. Indeed, the size of CDR modelled by the IPCC has decreased by approximately 20% since the Special Report on 1.5°C (in pathways that limit warming to 1.5°C with no or limited overshoot), and AR6 pathways designed to limit temperature overshoot rely less on net-negative emissions, and therefore CDR technologies, in the long- term (chapter 3.4.7, table 3.5).

Currently, only afforestation and reforestation are widely deployed. However, the carbon stored by these methods can be removed by human intervention at the project level (such as logging) and is vulnerable to natural loss (e.g. through forest fire or disease) (SPM C.11.3). The AR6 WGIII report stresses that while the land sector will be crucial to mitigation, it cannot compensate for delayed emission reductions in other sectors (chapter 7, executive summary). Given that the AR6 WGI report found that land sink efficiency is decreasing with climate change, relying too much on land to remove CO2 from the atmosphere could be problematic. This is key, as many corporations are relying on offsetting emissions in the land sector instead of reducing them. Scenarios that model stringent demand-side mitigation, energy efficiency, recycling, telework, travel avoidance, waste reduction and less meat-intensive diets have been shown to reduce dependence on CDR and reduce pressure on land (chapter 3.4).

There has been “fervent debate” on the use of bioenergy with carbon capture and storage (BECCs) in mitigation scenarios (chapter 3.2.2). Reliance on BECCs has been criticised for causing biodiversity loss, undermining food security, creating uncertain storage potential, excessive water use as well as creating the potential for temperature overshoot (chapter 3, box 3.4). The overall land dynamics of bioenergy production and afforestation is modelled to take place in tropical regions where land for dedicated bioenergy crops and afforestation displace agricultural land for food production (cropland and pasture) and other natural land. For example, in the 1.5°C mitigation pathway in Asia, bioenergy and forested areas together increase by about 2.1 million square kilometres – an area the size of Saudi Arabia – between 2020 and 2100, mostly at the cost of cropland and pasture (chapter 7, figure 7.14). BECCs is also typically associated with delayed emissions reduction in the near-term (chapter 3, box 3.4).

The Indonesia Just Energy Transition Partnership (I-JETP) is a landmark climate finance agreement reached between Indonesia and a group of…

Key points: The International Monetary Fund (IMF) and the Multilateral Development Banks (MDBs) play a crucial role in providing climate…